- The GTVC Publication

- Posts

- The Search for Liquidity: Why Modern Portfolios are Shifting Toward REITs

The Search for Liquidity: Why Modern Portfolios are Shifting Toward REITs

The GTVC Publication: Edition 8 -- Authored by Zachary Reed

GT Venture Capital Club

March 19, 2026

In an era of diminishing returns in private markets, the most valuable asset in a portfolio is no longer the one that grows the fastest. It is the one that you can actually turn into cash.

The most lucrative corner of the market is often not where everyone is already positioned. Investment management is a constantly evolving landscape where the most critical task is identifying which asset classes align effectively with your portfolio strategy. As an individual investor, you should look to evaluate not only the potential for a high return, but also factors such as risk exposure and asset liquidity.

Although private equity (PE) has historically generated strong returns, it has become detrimentally overcrowded. The recent influx of interest within this space has led to inflated market expectations and reduced asset liquidity, significantly diminishing PE’s relative attractiveness in the world of investment. This has urged investors to pivot towards publicly traded Real Estate Investment Trusts (REITs) as a more liquid, transparent, and accessible alternative.

The Decline of Private Equity

Although private equity is defined by high barriers to entry, the asset class has still faced overcrowding in recent years. This interest is driven by a decade of historic outperformance and an increasing supply of private companies that are ripe for “flipping”. While a flood of interest implies an increase in capital required for larger acquisitions and may seem beneficial, it has actually triggered a negative trend for this asset class.

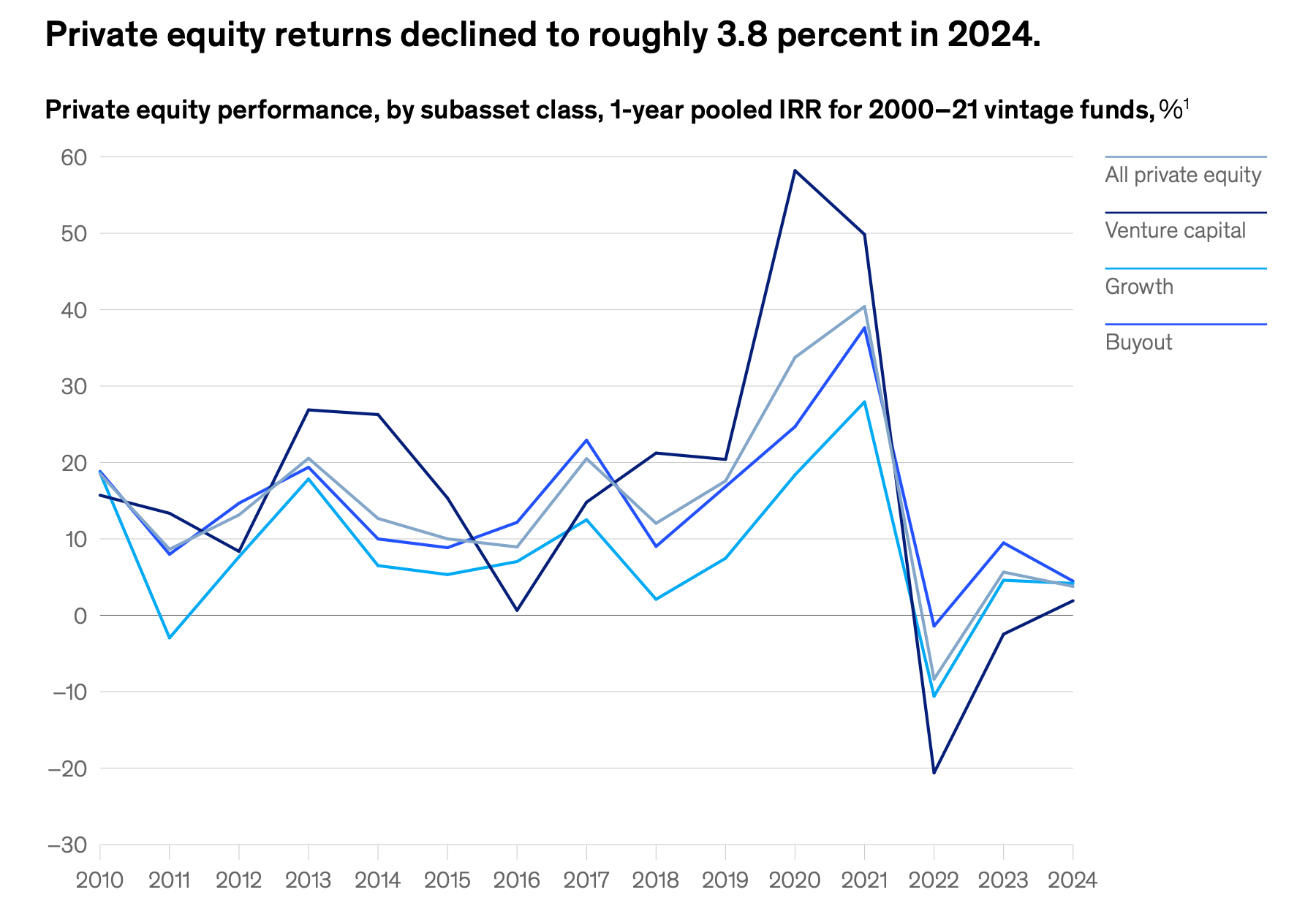

Figure 1 — Source: McKinsey & Company

This negative trend is primarily due to irrational market expectations. Many investors have come to expect 10x - 15x annual returns out of PE, which is unfortunately not sustainable in the currently saturated market. In reality, the surge in demand within this space has created an imbalance.

The pace of mergers and acquisitions (M&A) and initial public offerings (IPOs) has slowed down because there are too many dollars chasing too few high-quality targets. This stagnation is reflected in Figure 1. Private equity returns declined to approximately 3.8% in 2024, demonstrating a shift away from the previous high-growth era.

What are Real-Estate Investment Trusts

A REIT is very similar to private equity in the sense that they both pool capital to acquire, manage, and eventually sell assets at a higher valuation. The main distinction between the two is that PE follows that model with private companies, while REITs focus exclusively on commercial real estate.

Unlike private equity, REITs are structured to provide stability and reliable cash flow. They typically hold properties for at least 2 years, generating consistent income through rent collection. Since several REITs are traded publicly, they provide a level of liquidity and transparency that is unmatched in the private markets

A common misconception when evaluating REITs is that you are investing directly in bricks and buildings. In reality, buying a REIT share means you are investing in a company that owns and operates those properties. This structure allows individual investors to gain exposure to commercial real estate (from data centers to healthcare facilities) without the burden of direct property management.

Advantages of REITs

As mentioned earlier, REITs offer a level of liquidity that private equity cannot match. This high liquidity, combined with their historical independence from traditional stock and bond trends, allows REITs to provide valuable portfolio diversification without the risk and lack of capital accessibility associated with PE.

Figure 2 — Source: ChartOfTheDay

Even when comparing them against traditional stocks as shown in Figure 2, REITs have been substantially ahead of the S&P 500 in terms of total return for the past 25 years. Besides benefiting your portfolio, REITs also have low capital intensity. This means that the common investor can easily enter the market, avoiding the high barriers to entry that come with PE.

Furthermore, REITs provide a tax advantage. The regulatory framework used to govern REITs establishes that in order for these companies to maintain their status, they must distribute at least 90% of their taxable income to shareholders. By eliminating the corporate-level tax layer, REITs can ensure that a much larger portion of the company’s income and capital gains flows directly into the investor's pocket.

The Case for REITs over PE

The choice between these two asset classes will often come down to your personal risk tolerance and the amount of capital at your disposal. While REITs are inherently dependent on the often tumultuous real estate market, they still offer a level of stability and transparency that is rarely available in private equity.

The recent cooling of the private equity sector is a result of funds struggling to find profitable exits for their investments amidst a liquidity crunch. This has led to record-high levels of holding periods that lock LPs into assets much longer than expected. Historically, PE has attracted high-net-worth individuals. But for the common investor, REITs present a far more reliable option.

Ultimately, investors are moving toward REITs because their accessibility, liquidity, and diversification better align with modern portfolio strategies. Even for high-net-worth individuals, the current oversaturated state of private equity makes the reliability of REITs an increasingly attractive investment. In an era of diminishing PE returns, the most valuable assets are those that can be reliably liquidated, such as REITs.

Find more posts from the Georgia Tech Venture Capital Club here:

Lead Editor of The GTVC Publication: Sash Vijayakumar